From the Sidelines

By: Ray G. Talimio Jr.

“Growth Must Outrun Debt.”

As of January 2026, the Bureau of the Treasury (BTr) reported that National Government (NG) outstanding debt reached eighteen trillion one hundred thirty three billion pesos (P18.13T). Of this amount, domestic obligations accounted for twelve trillion three hundred twenty five billion pesos (P12.32T), while external debt stood at five trillion eight hundred nine billion pesos (P5.81T).

The increase since 2022 has been substantial. At the end of 2022, NG debt stood at thirteen trillion four hundred nineteen billion pesos (P13.42T). The rise to P18.13T represents an expansion of four trillion seven hundred ten billion pesos (P4.71T) in a little over three years, reflecting persistent fiscal deficits and continued reliance on borrowing to finance spending.

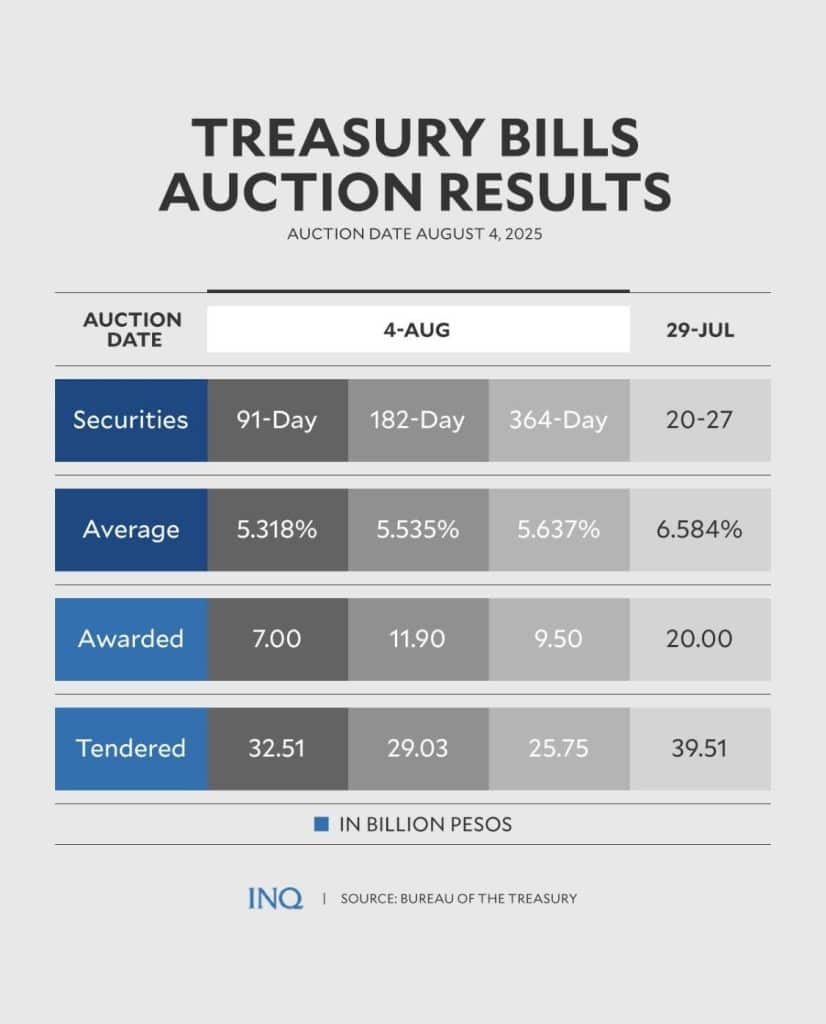

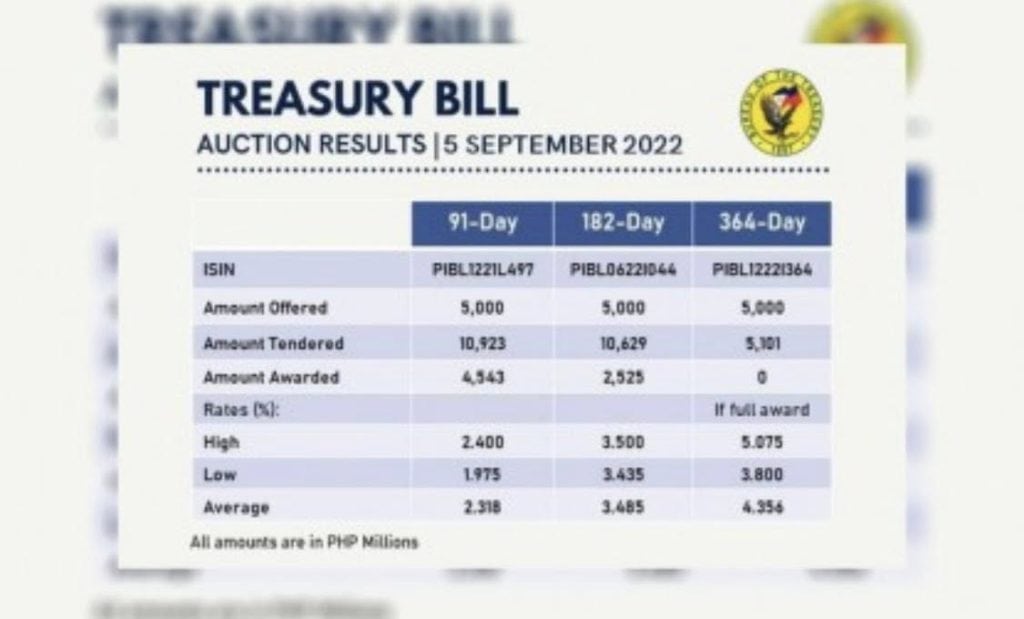

Domestic borrowing remains the dominant component of the debt structure. Treasury Bonds and Notes account for eleven trillion three hundred seventy five billion pesos (P11.37T), while Treasury Bills represent nine hundred fifty billion pesos (P0.95T) of the domestic stock. These government securities are issued regularly through BTr auctions and are purchased mainly by banks, institutional investors, and pension funds.

Debt servicing is becoming a larger budget item. In the 2025 General Appropriations Act (GAA), the Department of Budget and Management (DBM) allocated eight hundred seventy seven billion pesos (P877B) for the debt burden, equivalent to 13.8% of the national budget. In the 2026 General Appropriations Act (GAA) totaling six trillion seven hundred ninety three billion pesos (P6.793T), the debt burden rises to nine hundred seventy nine billion pesos (P979B), or about 14.4% of total spending.

Equally important is the debt-to-gross domestic product (debt-to-GDP) ratio, which has climbed to about 63%, breaching the commonly cited 60% threshold used by investors and credit rating agencies as a reference point for fiscal sustainability. Crossing that level does not automatically mean a crisis. Many countries operate above it. However, it does signal that the country’s fiscal position is becoming more sensitive to deficits, borrowing costs, and economic shocks. When the ratio remains elevated, markets pay closer attention to government spending discipline, revenue performance, and the quality of public investments. Credit rating agencies also factor this into their assessments because a rising debt ratio can affect the country’s borrowing costs and long term credit outlook. In practical terms, the higher the debt relative to the size of the economy, the greater the pressure on the national budget to allocate resources for interest and debt servicing instead of development priorities.

Sources:

Bureau of the Treasury (BTr), National Government Debt Indicators, January 2026; Department of Budget and Management (DBM), FY 2025 and FY 2026 budget documents.

Photo Credits:

Bureau of the Treasury building photo (file photo); Philippine Daily Inquirer (Inquirer) Treasury Bills auction results infographic using BTr data; BTr Retail Treasury Bonds campaign graphics; BTr auction materials.

Disclaimer:

This column reflects the personal analysis of the author based on publicly available fiscal data and is intended for public policy discussion.

About the Author:

Ray G. Talimio Jr. is a Certified Public Accountant and veteran columnist on governance, economic policy, and public accountability. He is a Past President and Past Chairman of the Board of the Cagayan de Oro Chamber of Commerce and Industry Foundation Inc., a former Co-Chairman of the Regional Development Council Region X Economic Development Committee, and a National Officer of the Philippine Institute of Certified Public Accountants. He also served as BIMP-EAGA Chairperson from 2023 to 2025 and is an active member of the Association of CPAs in Public Practice (ACPAPP).

###